Rated 4.9+ stars by

verified, happy customers

When a senior loved one needs help at home, one of the first questions families ask is "How are we going to pay for this?" The emotional weight of seeing someone you love struggle with daily tasks collides with the financial pressure of affording care. You're not alone in feeling that tension.

Of all the seniors currently living at home, 60% want to age in place with a caregiver, but only 37% feel confident it will actually happen. The gap between what people want and what feels financially possible is real, but it's not insurmountable.

Most households use a combination of private resources and assistance programs rather than relying on just one funding source. The key is knowing what's out there and which options the person receiving support qualifies for.

Village Caregiving explains how to pay for home care and the realistic costs. Whether you're planning ahead or responding to an urgent need, you'll leave with a clear picture of what's possible.

Before you can evaluate ways to pay for in-home care, you need a realistic number to work with. Costs vary significantly depending on where you live, the type of support you need and how many hours are required each week. Knowing the baseline helps you plan.

Nonmedical in-home care is a type of support that includes:

The national median hourly rate for nonmedical caregiver services was $35 per hour in 2025. At 44 hours per week, that works out to roughly $80,080 per year. The more hours required, the higher the annual cost.

The hourly rate varies between states. Wyoming has the highest rate at $46 per hour, while Mississippi has the lowest at $24 per hour. Urban areas within a state often cost more than rural regions. When budgeting, use your specific state's median rate as a starting point, then adjust based on local agencies' pricing.

Skilled home health services are a separate category from nonmedical support. This level involves licensed medical professionals — nurses, physical therapists, occupational therapists or speech therapists — delivering treatment ordered by a physician. These services address medical needs like wound management, medication oversight, post-surgery recovery or rehabilitation after a stroke or injury.

Since these home healthcare services require licensed clinicians, they cost more than nonmedical in-home care. The 2025 national median was $90 per hour for private nursing in the home or $160 per visit, depending on the medical needs. This information is important for budgeting, and because Medicare coverage rules apply differently here than to nonmedical support.

Many people wonder how in-home support stacks up financially against assisted living or nursing home placement. The answer depends on the level of supervision and medical attention your senior loved one requires, along with how costs are structured.

National median costs for different settings in 2025 include:

Round-the-clock supervision or extensive medical treatment may make a nursing home more cost-effective for some individuals. However, those who need moderate support with daily activities and want to remain in their own home often find nonmedical in-home services more affordable, especially when paired with family caregiver involvement. The costs of aging in place extend beyond direct service expenses and include home modifications, transportation and other support, so it's worth evaluating the full picture.

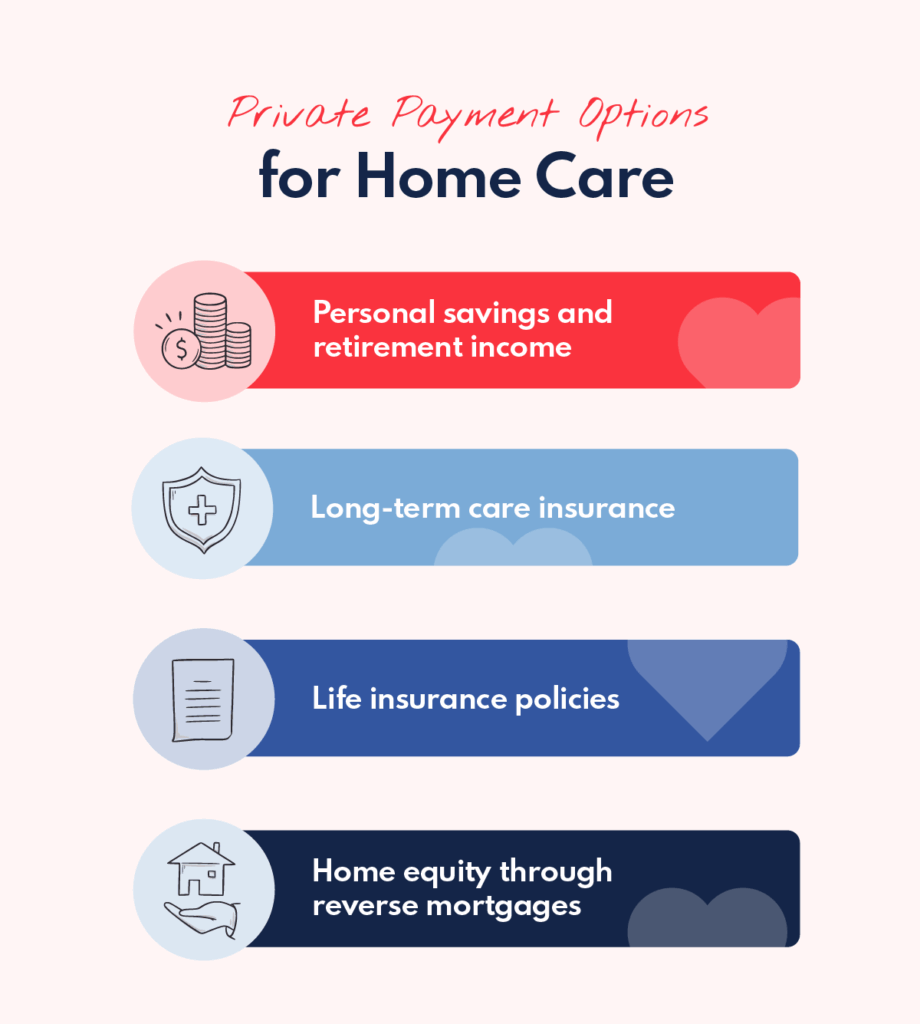

Most people begin with personal resources and work outward from there. Private funding typically comes from one or more of four main sources:

Many households use a combination rather than relying on a single option.

Personal savings, retirement income and pooled contributions from siblings or extended relatives are common starting points. Only 21% of adults 65 and older have long-term care insurance, so most draw on private funds as their primary resource.

Predictability helps when budgeting from savings. Some agencies offer flat-rate pricing, which means the hourly rate stays the same on nights, weekends and holidays. This structure makes it easier to forecast monthly costs and avoid surprise bills. If you're comparing providers, ask whether they charge flat rates or variable pricing based on the time of day.

Long-term care insurance is designed specifically to cover the cost of services as you age. People typically purchase these plans in advance and pay a daily or monthly benefit toward qualifying expenses, including in-home support, assisted living or nursing home placement.

Coverage terms vary widely. Key factors to evaluate include:

Premiums have risen in recent years, and plans become harder and more expensive to obtain after age 60 to 65. If coverage is already in place, review the documents carefully to see whether your insurance pays for home care, what's included, how to file a claim and whether there are restrictions on which providers you can use.

Existing life insurance can be converted into a source of funds in two main ways:

Some contracts also include accelerated death benefit riders, so you can access a portion of the payout while still living if certain qualifying conditions are met, such as a terminal illness or the need for long-term support. Review the documents to see what options are available, and consult a financial advisor before making changes that could affect beneficiaries or create tax implications.

Accumulated home equity becomes a funding source for seniors through reverse mortgages, which eliminate traditional monthly payment obligations and allow continued residence in the property. The Federal Housing Administration insures the home equity conversion mortgage (HECM), which accounts for most of these transactions.

To be eligible, you need to:

The loan can be structured in three ways:

Repayment is due once the borrower vacates the residence permanently — through death, relocation or sale. Most often, heirs sell the property to cover what's owed, which reduces their inheritance. The debt also increases throughout the loan term as interest accumulates.

Reverse mortgages can be useful for unlocking equity, but they come with risks and fees. It's worth consulting a financial advisor or housing counselor approved by the U.S. Department of Housing and Urban Development before proceeding.

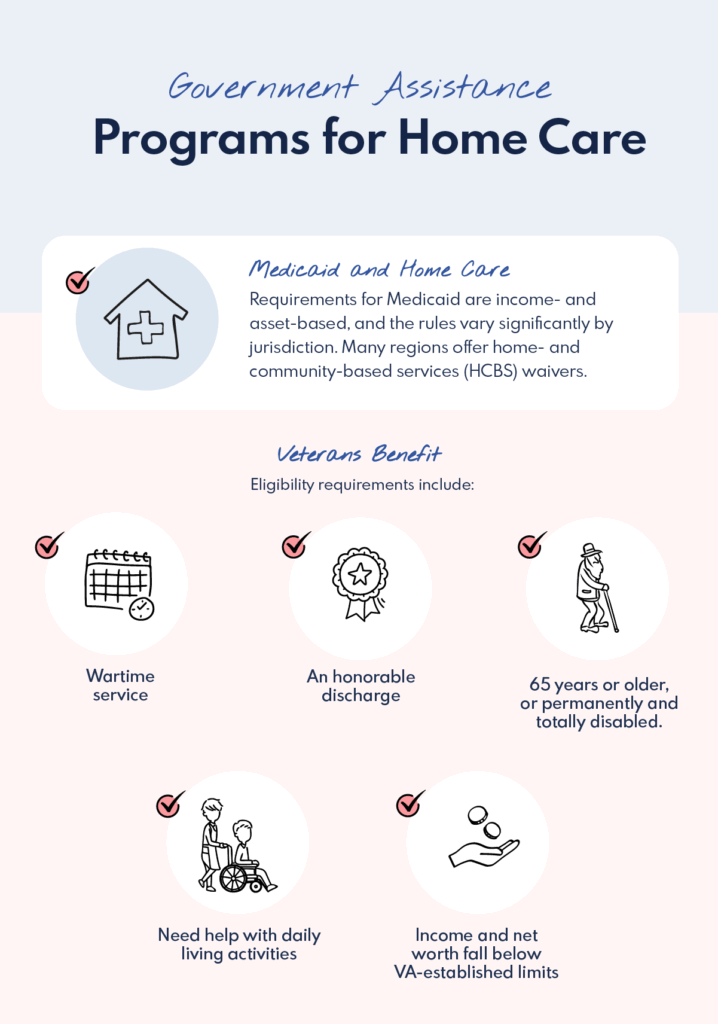

Two main government programs — Medicaid and VA benefits — can help qualifying seniors offset or significantly reduce costs. Both have income and asset requirements, and rules vary by jurisdiction or individual circumstance. Checking your specific state's programs and veteran status is an important step in the planning process.

Medicaid is the primary government program that covers nonmedical in-home support for those who meet income and asset thresholds. This program differs from Medicare, which covers skilled home health services only when they're medically necessary and ordered by a physician, such as nursing or physical therapy following a hospital stay. Medicare doesn't cover ongoing, nonmedical assistance like personal help, companionship or daily activity support.

Requirements for Medicaid are income- and asset-based, and the rules vary significantly by jurisdiction. Many regions offer home- and community-based services (HCBS) waivers, which are designed specifically to fund in-home support as an alternative to nursing home placement. Thresholds, covered services and waiting lists differ from one area to the next, so it's important to check with your local Medicaid office or consult an elder law attorney for current rules.

The U.S. Department of Veterans Affairs (VA) Aid and Attendance benefit is the primary program for funding in-home support for those who served. It's an add-on to the VA Pension and is paid monthly as cash directly to the recipient or surviving spouse. The funds can be used to pay for in-home assistance, assisted living or other expenses as needed.

The key eligibility requirements include:

The net worth limit is set at $163,699 from December 1, 2025, to November 30, 2026. These rates are adjusted annually for cost-of-living increases. Unreimbursed medical expenses can be deducted from countable income when calculating qualification. This means that paying for support out of pocket may actually help more people meet the threshold. Surviving spouses of those who served can also apply.

Whether you're planning proactively or responding to an immediate need, taking a few concrete steps now can make the financial picture clearer and more manageable:

Remember that preparation also includes physical modifications — grab bars, ramps or accessible bathrooms — to the residence, and only 10% of American homes are “aging ready.” Many physical modifications require advanced planning and funding to implement.

For those managing from a distance, long-distance caregiving resources can help coordinate services. When you're ready to evaluate providers, choose a home care provider that can clarify what to look for in terms of services, pricing and reliability.

The path forward looks different for every household. The best option depends on the level of support required, the financial resources available and which programs the person qualifies for. Starting the conversation early, before needs become urgent, is the most important step. Assess what's needed, estimate realistic costs based on your location and explore every available funding source simultaneously, rather than waiting to exhaust one option before moving to the next.

Consult with a financial advisor or elder law attorney to help you navigate Medicaid requirements, protect assets and make informed decisions about insurance and equity. This is a challenging process, but it's manageable when you have the right information. Millions navigate these decisions every year, and most find a path forward by combining resources creatively.